Background:

In the uranium market, there are three large western converters where most trading and physical delivery of material take place: Cameco’s Port Hope (“CMC”) in Canada, ConverDyn’s Metropolis (“CVD”) in the United States and Orano’s Comurhex (“CHX”) in France. Historically, uranium for delivery at each location was priced relatively tightly (say $0.10 – $0.50) with CHX and CVD trading at slight premiums due in part to transport and tax considerations. Today, that spread is approximately $3.00 – 4.00 with CMC trading at $34 and CHX/CVD closer to $30. The size and duration of this spread has confused both market participants and investors over the last couple months. There is a simple argument that some have made – the spread implies that because of their spot purchase program, Cameco is artificially pushing up CMC and that the “real” price of uranium is closer to the $30 quoted at the other locations. The point of this blog post is to peel back the onion a bit and walk through some of the more nuanced dynamics in the physical market to explain what is taking place.

An Argument for Discounts at ConverDyn & Comurhex

As stated above, some have recently argued the CMC price of uranium is artificially inflated vs. CVD / CHX. But could it be that there are reasons for CVD / CHX to trade at a substantial discount in today’s market? We think so.

For those that do not follow the conversion market closely, ConverDyn is a general partnership between two large multinational companies Honeywell International and General Atomics. In late 2017, Converdyn announced that it would suspend operations at Metropolis due to market forces (i.e., price). So today, you can take delivery of material at CVD but you can’t convert it there. Another wrinkle is that significant material was moved to CVD during 2018/2019 as market participants attempted to pre-position inventory in the United States ahead of the Section 232 / Working Group decisions (with the assumption material already in the U.S. would be grandfathered regardless of origin). So today you have artificially inflated levels of inventory at CVD but you can’t actually convert that material as the facility remains offline with no guidance for a restart (which in and of itself will be a lengthy process).

The logical next question would be – why doesn’t a trader just buy at CVD and transport to CMC to close the arb? This is where the uranium market differs from many commodities – you can’t just rent a truck and cross an international border with radioactive material. When market participants agree to store material at one of these facilities, they also agree to limitations on how that material can be transported. If Metropolis were up and running it would normally be staffed with employees who could move that material and close the arb, but those employees are currently furloughed. Why doesn’t Honeywell hire a few people to take advantage of the current situation? While making a few million dollars on the spread may seem like a lot of money, Honeywell is a company with ~$35 billion in revenue – they are not adjusting operations at a closed facility for a quick trade and relatively small payout. So today if you are a trader and you want to close the gap by physically moving pounds out of Metropolis, you can’t! For the time being those pounds are stranded and cannot be converted – for that reason, a discount is warranted.

Moving on to CHX in France, readers should know that while the new Philippe Coste conversion plant at Orano’s Tricastin site was commissioned in late 2018, it is nowhere near full capacity and ramp up has been considerably delayed. While they may reach full capacity sometime in 2021, these delays have led to an overstocking with some reports that they are physically running out of storage (what happens when completely full? We’re not actually sure). Additionally, we have received word that Orano distributed a relatively broad Force Majeure letter in March as a result of COVID-19. We have not heard of material actually being impacted by the virus in France but if not rescinded, utilities and traders are clearly taking additional risk by accepting and storing material at these facilities relative to CMC.

What is clear is that if you want to buy and actually convert your material today, your best (or only?) bet is CMC. From a fundamental perspective it makes sense that material at CVD / CHX would be discounted.

Buying Seasonality & Trader Pricing Factors Impacting the Spread

We do acknowledge that the majority of trading at the moment is being driven by producers and market intermediaries. This is actually not surprising given the violence of the recent move in spot and the general seasonality of utility fuel buying. We have seen some fuel buyers postpone activity which was expected in the spring – this may have been due to COVID-19 considerations at their plants or a feeling that they didn’t want to “chase” a rising market until they knew it was real. Either way – the late spring / early summer is typically a quiet time for end user demand. Most buying interest tends to pick up in late August into the WNA Symposium the first week in September and then accelerate through the fall. This year will likely be a bit different as you will have additional spring demand pushed into the fall making it more active.

Meanwhile with McArthur River and Cigar Lake shut down, producers who typically use those pounds to fulfill long term contract obligations have become the main buyers (and not surprisingly are short those pounds in Canada). This means the main source of demand during a seasonally quiet period is all sitting in one place, driving a justified premium for pounds near term at CMC. One interesting point is that we are also seeing some traders try and pull forward pounds to meet that near term demand, which explains the shape of the curve on the short end and likely leaves us with a thinner market later in the year (right when we expect utility fuel buying to pick up).

One other interesting point is that the location spread may actually be widening as a result of how some offtake contracts with traders are structured. The best way to describe this dynamic is with a hypothetical example:

Trader X has an offtake agreement whereby they receive material at a specified discount of 3-5% to spot, with spot defined in this example as the Broker Average Price (“BAP”) as reported by UXC. This offtake could be from a known producer electing to sell through traders for anonymity (Uzbekistan, BHP, etc.) or, many times could be a JV partner to a large producer who receives their portion of material from a project but does not actively trade the commodity (i.e., they need the trader for market access – an example could be ONAREM, the Niger Government’s JV entity for Somair). While most utility contracts give the buyer optionality over point of delivery, not all offtake contracts have that flexibility meaning that in this example, the point of delivery is fixed at CHX in France.

Normally the trade is relatively simple – trader receives material at CHX at a 3% discount to spot and then sells it in the spot market and clips that spread as payment for market access. Even if there is some spread between locations, the agreed discount typically gives them plenty of flexibility given that the spread between UXC’s BAP and CHX is very close (maybe a $0.05 – 0.15 spread vs. the $0.90 implied in their 3% discount assuming $30 uranium).

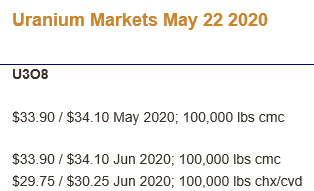

Today is different. Today UXC’s BAP has been sitting much closer to CMC’s pricing reflecting that most real demand is occurring at that location. This can be a disaster for a trader receiving material under offtake at CHX and paying BAP closer to CMC. In our example, that trader pays ~$34 for material as quoted by BAP but receives material only worth $30 at CHX (see screenshot from this morning’s Uranium Markets trader run below). Suddenly their 3-5% spread comes nowhere near compensating them for taking location risk and they are under water on delivery.

We also should keep in mind that uranium is a small market where most traders are keenly aware of what others are doing. For that reason, traders likely understand that someone receiving an offtake at CHX in this environment wants to get rid of that material quickly to limit their loss on the trade (what happens if the spread continues to widen while they are paying BAP and receiving CHX?). For that reason, without steady end user demand at CHX, traders are incentivized to drop their bids as loose offtake material enters the market, thereby exacerbating the spread between locations.

Logical questions that follow from this example: why are we seeing so much volume trade at CHX? Why has BAP remained so much closer to CMC rather than showing an average of the three locations?

We think a lot of the volume quoted at CVD / CHX over the past couple months have been traders churning material (trading back and forth with each other) in order to make a volume argument to price reporters (UXC / Trade Tech) that their quoted prices should detach from CMC and reflect an average of different locations. To their credit, price reporters have seen through that argument and have generally kept quoted prices much closer to CMC where they are seeing real trading and delivery take place.

The other large question: Why isn’t Cameco trying to close the spread themselves? They could buy material at ConverDyn more cheaply and move it to their own facility (they are in the transport business). Our take is that as long as CVD pounds remain stranded, it further tightens the spot market which helps their negotiating position. Also – remember that Cameco sells conversion in addition to uranium and to the extent that premium uranium prices result in more material being moved to their facility (as traders with delivery flexibility move pounds to take advantage of premium pricing), it strengthens their ability to sell conversion for those pounds.

Implications and What We’re Watching

At first glance the current location spread in the uranium market may look like a simple aberration with potentially negative implications, but as we have tried to show there is far more going on beneath the surface. The most likely way for the spread to close is if fuel buyers with discretionary purchases elect to play the arbitrage. If they have inventory at CMC and are confident that Metropolis will be up and running in a couple years, they could be willing to take the risk of owning stranded rather than mobile material today (although we’d note that COVID-19 has highlighted the criticality of mobility/accessibility in the fuel cycle). Keep in mind that these are not nimble arbitrage traders playing for a quick buck. Some of the fuel buyers we have spoken with have actually shown more respect for the market – highlighting that the spread must be there for a reason (“I mean if it were free money, wouldn’t the traders be arbing it?”). Is it a certainty that utilities elect to use balance sheet to monetize this disconnect or is there a risk that they elect to follow the market, moving spreads even wider as we head to the fall? We’re not sure but we think following these dynamics are important as we get to the third quarter and the real buying begins.

One quick comment on the physical holding vehicles. We have seen some questions on why Yellowcake has not just sold their material at CMC and bought material at CVD, thereby enhancing NAV. First, this is a logical fallacy – their current pounds are worth ~$34 at CMC and they would be trading those for equivalent pounds worth ~$30 at CVD and $4/lb cash. The only way this would create value would be if the price at CVD then rises to match CMC which as outlined above may happen but is far from a certainty in the short term. You could argue that as a holding vehicle with no immediate need for pounds the gamble is still worthwhile – we’d just note that Yellowcake has traded at a 20-30% discount to NAV (~$100mm in mkt cap) lately and we’re highly skeptical that adding even $5-10mm to that value via an arbitrage trade really changes the value proposition for investors. Their discount is simply a function of having more sellers than buyers in a relatively illiquid stock – when that changes you’ll see the NAV discount disappear (and it will likely trade into a premium as holding vehicles have done in past rising uranium price environments).

Finally – to the extent you are invested in this space and you haven’t been focused on the Russian Suspension Agreement renegotiation, you should. It will likely be the most impactful catalyst for uranium in the second half of the year – we’ll likely release more on that topic in the future.

Thanks for reading,

Segra Capital Management